6 November 2020

The Market Place

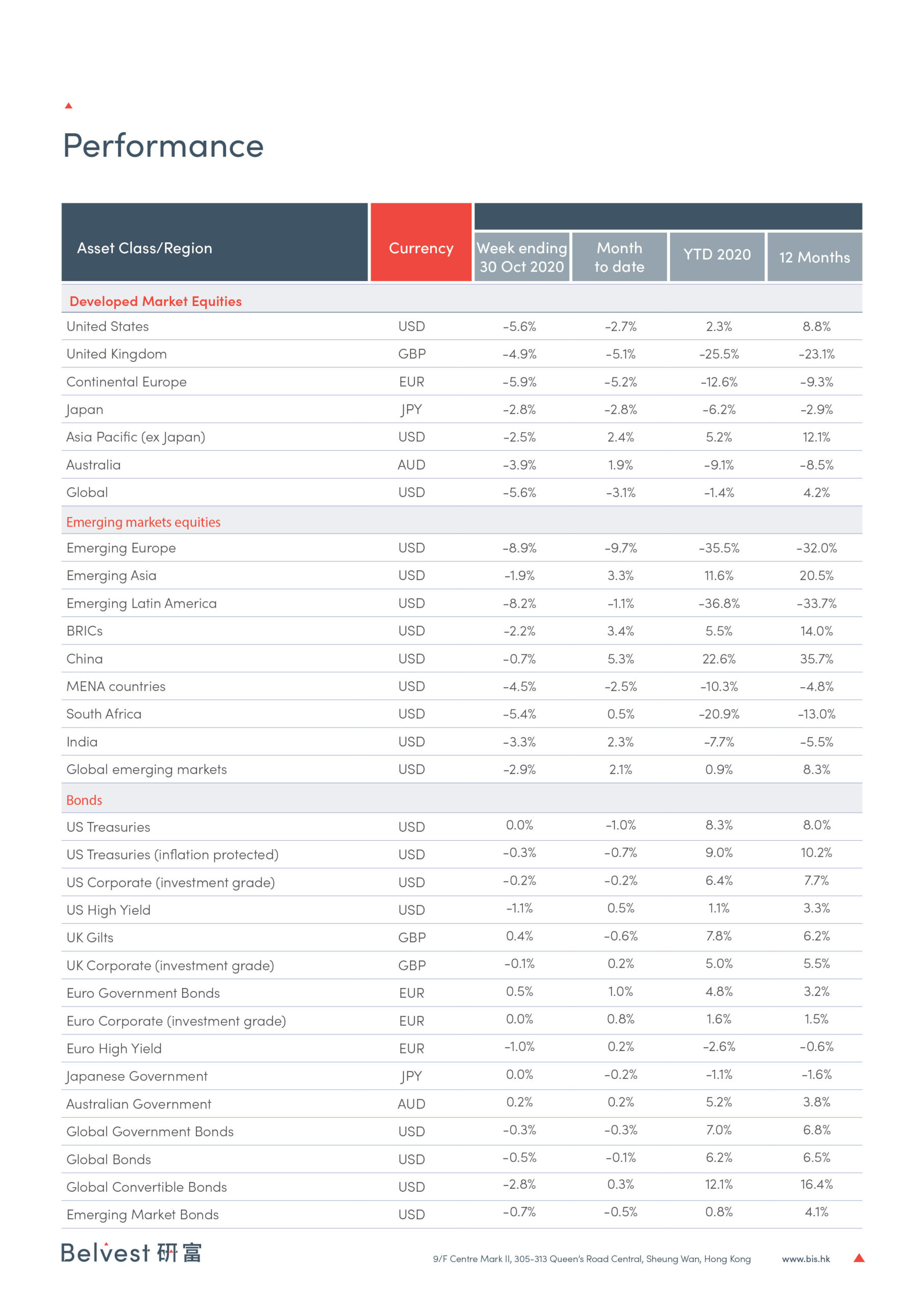

- Global equities fell -5.6% on the week as the number of Covid-19 cases surged in Europe and the US

- The US economy expanded at a record 33.1% annualised rate in Q3, which beat market expectations

- Brent crude fell -10.3% ending the week at $37.5 a barrel

- Gold fell -1.2% to end the week at $1878.8 an ounce

US

- The large-cap US equity benchmark returned -5.6% over the week

- An agreement on the latest round of fiscal stimulus has not been reached before this week’s presidential election

- September’s reading of the Chicago Fed National Activity Index was 0.27 against 1.11 last month, indicating that growth has slowed significantly, though it is still positive

- New home sales in September totalled 959k, down from 994k in August and well below the expected figure of 1,025k

- Weekly initial jobless claims were 751k in the week ending 24th October, down 40k from the previous week. It was the lowest initial claims total since the week of March 14th, when they came in at 282k.

Europe

- The main continental European equity index returned -5.9% last week

- France, Germany, Belgium and Greece have become the latest countries to announce second lockdowns.

- Preliminary official data indicates that Eurozone GDP grew 12.7% in the third quarter, after contracting -11.8% in Q2

- The ECB meeting saw monetary policy left unchanged and a unanimous post-dated decision made to act at the next meeting in December

- October’s Euro Area manufacturing PMI came in at 54.4 against 53.0 expected, while the services PMI was 46.2 against 47.0 expected

- Germany’s manufacturing PMI was 58.0 against 55.0 expected

UK

- UK equities fell -4.9% on the week

- Intense Brexit negotiations continued over the weekend, as substantial progress was made last week but divisions over issues such as fishing rights remain. Both sides are hoping that the ratification process will be started by mid-November

- England will enter a month-long national lockdown beginning on the 5th November

Rest of the World / Asia

- Global emerging markets fell -2.9% last week

- South Korea’s Q3 GDP came in at 1.9% quarter-on-quarter, against 1.3% expected

- China released details of its new five-year economic plan, which aims to make the country technologically self-reliant.

- China reported that profits from the industrial sector grew approximately 10% in September year-on-year, driven by electronic equipment manufacturing

- The Bank of Japan lowered its growth outlook for the remainder of the fiscal year and kept interest rates unchanged

It has been one of the main discussion points of the past three years, five years and even decades in the case of Japan: will inflation return? Low prices and ultra-low rates must surely end at some point; or maybe not… We are amid a pandemic and going through a period of depressed economic activity, so why would inflation even register on investors’ radars? As an asset allocator, it is imperative we consider what might happen to inflation and inflation expectations in the coming years in order to effectively build robust portfolios for our clients.